Are you seeking a solid reason to develop a digital wallet akin to Apple Pay? But what if you could go one step further? Consider launching a trendsetting bankless solution. It rivals the convenience of the big players and eliminates banks from the buyer-seller relationship.

Yet, innovation comes with its hurdles. The path to building a successful e-wallet without a bank account is a true riddle. It poses countless questions about security, perks, user adoption, and legal adherence, among others. In this Q&A guide, we'll explore these complexities in detail so that you can develop your own solution with confidence. Off we go!

written by:

Alexander Arabey

Director of Business Development

Contents

Q1: How Can Digital Wallets Unbank Us?

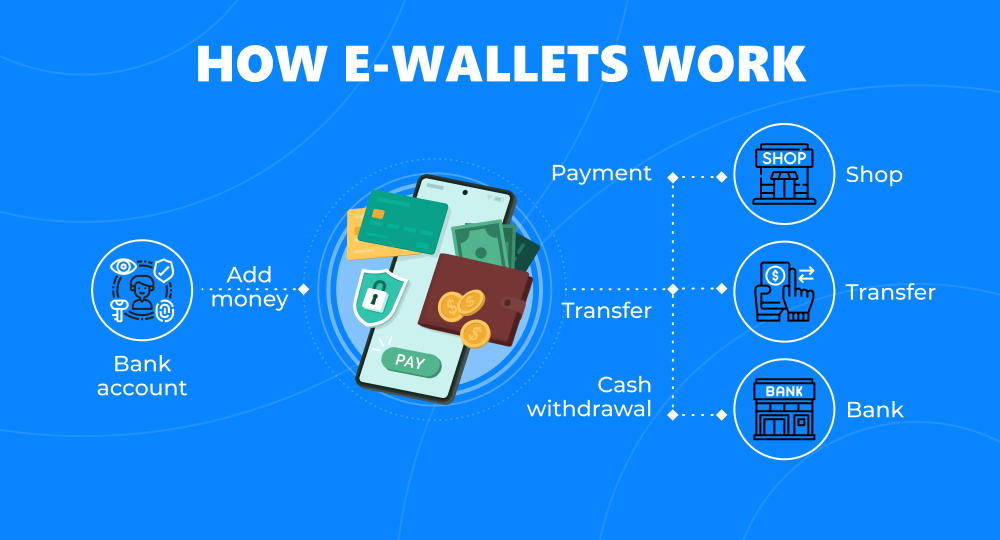

A digital wallet functions like a bank account, allowing users to store money virtually. Is it available to those who don't have bank accounts? To find out, let's explore how e-wallets operate.

Classic money transfer services such as Google Pay, Samsung Pay, and other digital wallets, work this way:

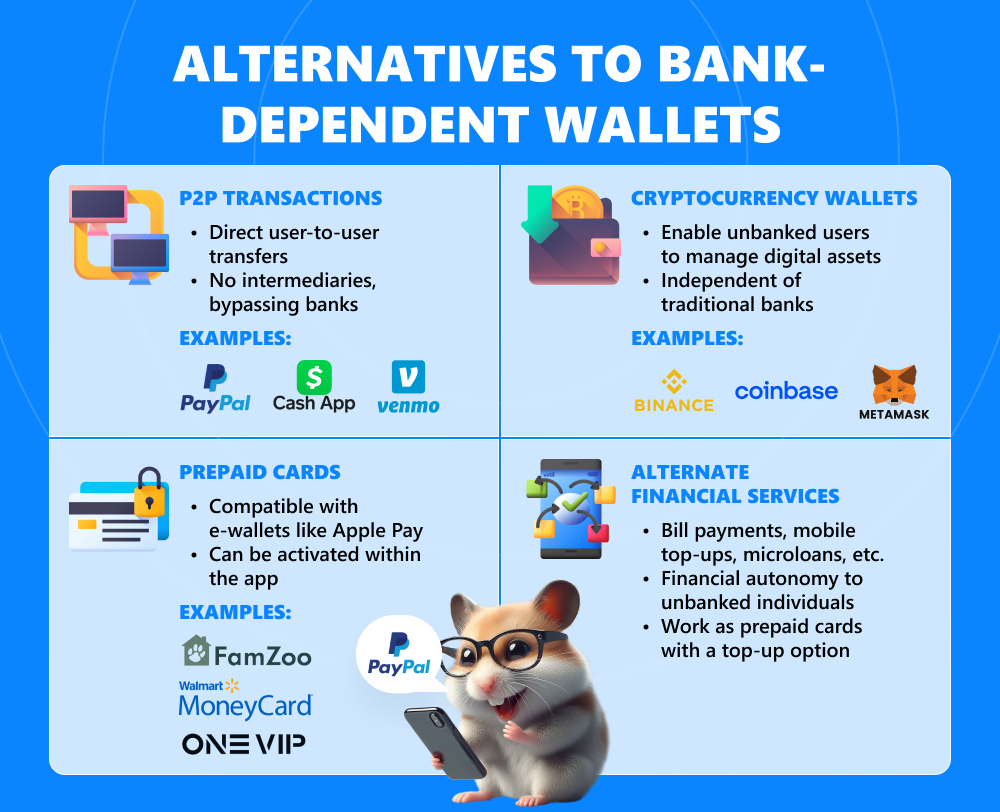

Simply put, they usually need a linked debit or credit card to function properly. Yet, there are alternatives to bypassing this requirement:

- P2P transactions. E-wallets allow for direct user-to-user transactions. People can transfer money to family, friends, or merchants without such intermediaries as banks.

Examples: PayPal, Venmo, Cash App. - Cryptocurrency wallets. They empower unbanked users to store and manage their digital assets independently of banks.

Examples: Coinbase, Binance, MetaMask. - Prepaid cards. Many prepaid debit cards (Visa, Mastercard, etc.) are compatible with wallets like Apple Pay. Users can add such a card to their wallet and activate it within the app.

Examples: Walmart MoneyCard, FamZoo Prepaid Card, ONE VIP by Visa. - Alternate financial services. Beyond traditional transactions, e-wallets offer bill payments, mobile top-ups, and microloans. This payment method grants unbanked individuals financial autonomy. All they need to do is load money into their e-wallet, like using a prepaid card.

Q2: What Are the Perks of an Online Wallet without a Bank Account?

Financial inclusion. E-wallets invite unbanked customers to use international money transfer services:

- Receive payments;

- Send money;

- Pay bills;

- Use loyalty cards;

- Store personal documents.

Convenience and speed. Online wallets provide quick and convenient access to funds right from smartphones. For instance, Western Union enables sending money to bankless users using just a mobile phone number. No debit card is required.

Global access. Digital payment apps work across borders. They permit international transfers without a local bank account.

Lower fees. Traditional banks often charge for their services, even basic ones. Mobile wallets incur far fewer expenses. Yet, keep in mind the potential hidden costs:

- Free payments often need both parties to use the same wallet;

- Extra services, like quick transfers, may cost money even with free wallets;

- Large transactions may require a bank account and KYC verification.

Want to see the whole picture? Explore our detailed guide on e-wallets.

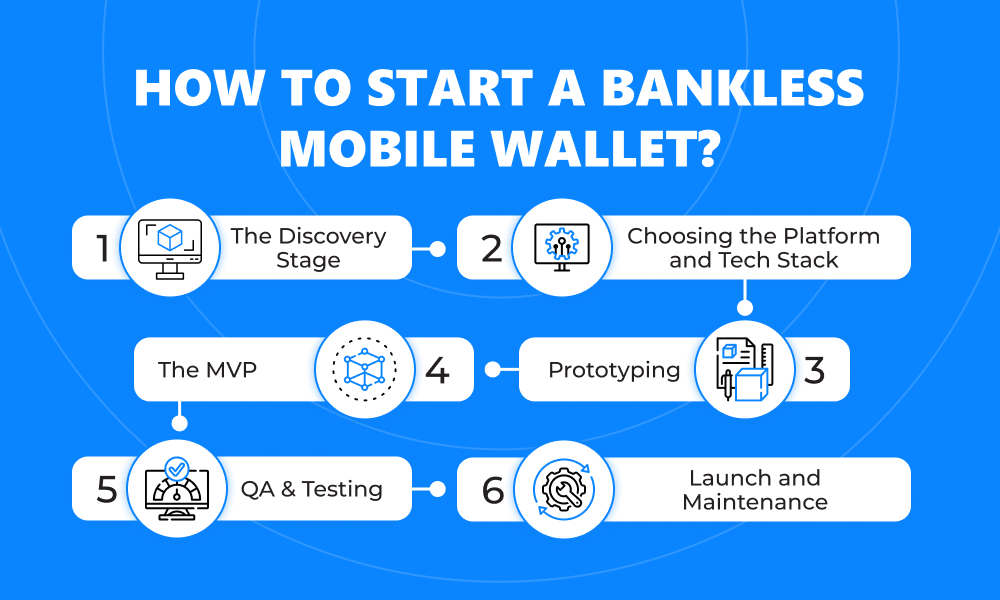

Q3: How to Start a Bankless Mobile Wallet?

Step 1. The Discovery Stage

It all starts with your idea. And then goes through these key phases:

- Understanding your audience. Who are your end users? Individuals, businesses, or both? Explore their pain points and the solutions they seek in your mobile wallet.

- Competitive market research. Who are your rivals? What makes their software thrive? Examine the market to craft a unique value proposition for your product.

- Defining essential features. While most e-wallets share common feature sets, focus on the core functionalities vital for your platform to win in the market.

Step 2. Choosing the Platform and Tech Stack

Decide between native and cross-platform options. Native apps offer specific mobile OS optimization but demand more resources. Cross-platform products are more cost-effective and easier to maintain, though less specialized.

How to choose wisely? Your business goals and tech requirements will drive your final decision.

For the tech stack, try to balance your project's size and complexity with the need for future scalability. The selected technologies should support your progress, not hinder it.

Step 3. Prototyping

A prototype visualizes your product concept. UI/UX designers develop wireframes of your wallet flow, mapping out the user journey. Such a proactive approach helps identify design flaws early on and avoid costly bug fixing later.

Once the design is approved, the focus shifts to fine-tuning the UI and UX for intuitive navigation and aesthetic allure.

Step 4. The MVP

Moving from concept to execution, your team will develop a Minimum Viable Product (MVP). This initial version should include fundamental features: diverse payment methods, fluid transactions, and a user-friendly design. After the launch, maintain a feedback loop with early users:

MVP → User feedback → Enhanced MVP → Further feedback → Progressive MVP

This iterative cycle promotes constant refinement of your app through user-driven enhancements.

Step 5. QA and Testing

Before debuting your digital wallet, undertake extensive testing. Thus, you'll identify performance flaws and user experience hiccups. Reach out to beta testers to fine-tune the app, ensuring a smooth rollout. Continuous Integration/Deployment (CI/CD) and methodical testing will confirm the app's quality and reliability.

Step 6. Launch and Maintenance

Make sure your wallet app adheres to all submission guidelines for the leading app stores: Google Play or the App Store. A well-planned PR campaign and partnerships with influencers can generate buzz before the big launch day.

Post-launch, the journey continues with ongoing maintenance. Regular updates, feature upgrades, and prompt customer support will keep your e-wallet relevant in the market.

Q4: What Are the Best E-Wallets without a Bank Account?

Name

OS

Pros

Cons

Ideal for

PayPal

Android, iOS, web

- Widespread adoption;

- Contactless transactions with Near Field Communication (NFC) and QR codes;

- P2P transfers;

- Crypto-friendly;

- The ‘Buy Now, Pay Later’ feature;

- Rewards program;

- Cash-back with select retailers and through the PayPal credit card.

- Complex fee structure;

- Possible account holds or freezes;

- Limited currency options;

- Challenges with resolving issues through customer service.

- Global consumers;

- Businesses;

- Mobile users;

- Frequent online shoppers;

- Millennials, and Gen-Xers.

Cash App

Android, iOS, web

- Ability to send cash, stocks, and crypto to any contact with a phone number or email;

- Zero fees in the UK;

- Intuitive financial management;

- Bitcoin rewards.

- Investment complexity

- A prime target for fraudulent schemes and scams;

- Mandatory account creation to accept payments;

- Withdrawal limits;

- Full functionality is limited to certain regions.

- Stock and cryptocurrency enthusiasts;

- Young adults;

- Tech-savvy individuals;

- Small business owners;

- Budget-conscious consumers.

Venmo

Android, iOS, web

- High transfer limits;

- Rewards with the Venmo Debit and Credit cards;

- Crypto-friendly;

- Social features, fostering a community experience;

- Instant money transfer service.

- By default, transaction details are visible publicly, which may raise privacy concerns;

- Social media overlap;

- Scam vulnerability;

- Limited international use;

- Fees for instant transfers.

- Young adults;

- Socially engaged users;

- P2P fans;

- Tech-savvy consumers;

- Small business owners.

Q5: How to Secure a Mobile Wallet?

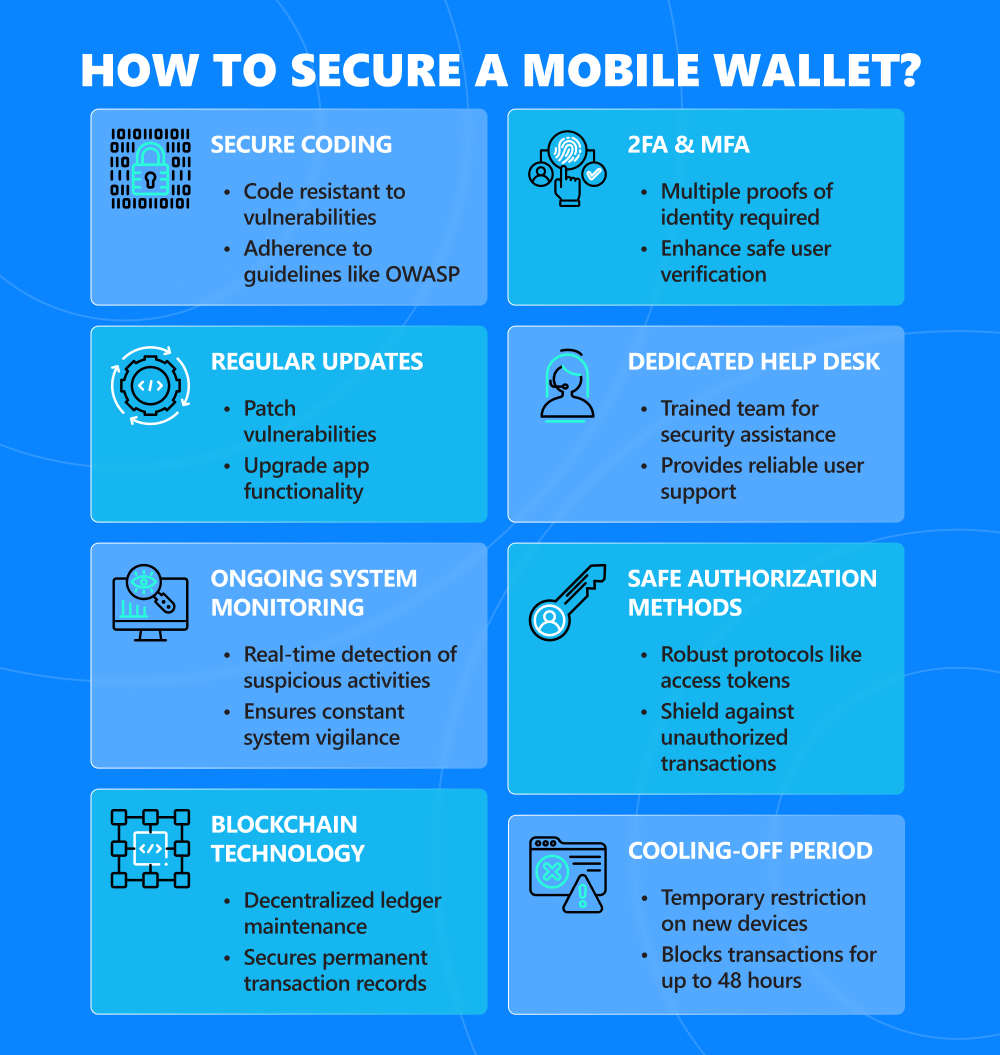

It's not enough to set up encryption measures within your app. To safeguard a mobile wallet from cyber threats, put in place a robust security framework with advanced practices. This may include:

- Secure coding. The foundation of your app's security is its code, resistant to common vulnerabilities and exploits. Make sure your development team adheres to secure coding guidelines, like OWASP, which prevent breaches.

- Two-factor & multifactor authentication (2FA/MFA). How to guarantee safe user verification? With 2FA or MFA. These methods need several identity proofs beyond a password, such as a fingerprint or a one-time code sent to a mobile device.

- Regular updates. They are necessary for patching vulnerabilities and upgrading functionality. This applies both to the virtual wallet app and its underlying infrastructure.

- Safe authorization methods. Set up robust authorization protocols, like access tokens, to protect against unauthorized transactions.

- Ongoing system monitoring. Use real-time monitoring tools to detect and respond to suspicious activities. This will guarantee constant vigilance over system security.

- A cooling-off period. It helps protect an account from unauthorized access or fraud. If a user logs in from a new device or in a less secure way, the app temporarily restricts sending and receiving money — usually for up to 48 hours. Any transactions within this limit will be automatically blocked.

- Blockchain. It uses a decentralized network of computers to maintain a ledger that is virtually impossible to alter without detection. This means that once a transaction is logged on the blockchain, it becomes part of the permanent public record.

- Dedicated help desk. Gather a responsive customer support team trained to assist with security concerns. Thus, you'll provide users with a reliable point of contact for anything from incident reports to suspected scams.

Final Reflections

The physical wallet, once a staple in our daily carry, now shares its esteemed place with its digital version — the e-wallet. This tool is more than convenient, but transformative. Fintech innovators are pushing humanity forward, offering mobile wallets for a myriad of operations:

- Instant payments;

- Dynamic currency exchange;

- Accessible microloans;

- Secure cryptocurrency management, etc.

What can make e-wallets even more convenient? Bank-independent operations. This is where the real business opportunity lies. Bankless e-wallets are the future, and they're ripe for investment. The challenge is significant: security concerns are the main barrier to mass adoption. Yet, overcoming this obstacle is not just a milestone. It's a statement of your company's commitment to innovation and trustworthiness.

Are you ready to challenge traditional banking and claim your stake in the digital ecosystem? Contact us for assistance on this bankless journey.

Contacts

Feel free to get in touch with us! Use this contact form for an ASAP response.

Call us at +44 151 528 8015

E-mail us at request@qulix.com

Feel free to get in touch with us! Use this contact form for an ASAP response.

Call us at +44 151 528 8015

E-mail us at request@qulix.com

![]()

![]()

![]()