Create a Digital Bank from Scratch

We know how to create a full-fledged digital bank, and we are good at it. Our portfolio includes more than 20 neobank projects in the capacity of a general contractor or a key partner.

Get the latest insights on the best way to transform your banking experience.

Get the latest insights on the best way to transform your banking experience.

Get the latest insights on the best way to transform your banking experience.

Get the latest insights on the best way to transform your banking experience.

We know how to create a full-fledged digital bank, and we are good at it. Our portfolio includes more than 20 neobank projects in the capacity of a general contractor or a key partner.

Building a neobank in the same way as a traditional bank will not work. Neobanks demand a brand-new approach. It has to be agile, iteration-oriented, with practical research of hypotheses, and rapid consideration of client feedback. Our team knows how to bring all that to life and do it within a year at a very reasonable pricing.

We can act as a general contractor on your neobank project. We are willing to undertake the integration of all components as well as other vendors into a single structure and be accountable for the achievement of business results.

Definition of the neobank concept, macro-planning, and the establishment of ICP/positioning.

Composition of the BRD. Joined by your team, our domain experts and analysts build and describe the necessary neobank processes.

Participation in negotiations with suppliers of external systems — GAP analysis, cost analysis, analysis of the implementation plan.

Realization of UI/UX, adaptation of business processes to project requirements and local legislation.

Deployment of an omnichannel digital banking platform and integration of all third-party components (more details here).

Coordination of activities related to the implementation of digital bank components and their refinement to meet the requirements (core, processing, CRM, KYC, etc.).

Pre-prod and production environment deployment (cloud or on-premise).

Full-fledged load and security testing.

Analysis of the early adopters' feedback and functionality adaptation.

Providing Tier-2+ support.

Please note that we do not provide core banking, card processing, and CRM functionalities. These components must comply with local regulations. From our side, we can advise on the suitable services providers and help you obtain the most favorable commercial conditions.

The platform encompasses a set of functional services that can be customized to meet the client's business requirements.

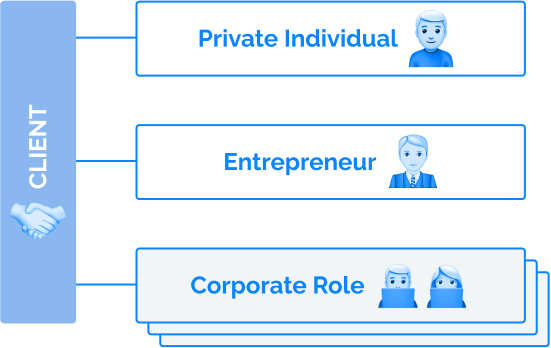

Support different customer profiles within one account. E.g., the user can be a private individual, an entrepreneur, a director at one company and a deputy director at another.

When developing a digital banking platform, we pay special attention to its easy and smooth integration with third-party services that extend the solution's functionality.

Our goal is to build you a quality product and make it hit the market as soon as possible. That is why we promote the MVP (a minimum viable product) first approach. This means that instead of spending years on the development of a full-fledged, feature-rich digital bank, you get the opportunity to present your tested and improved application to users within 6 to 12 months. The rest of the functionality will be implemented in the future — no rush, no risks.

Compulsory licensing

(Un)availability of a partner bank

Who the target audience is and how it affects the functionality and staging

Which solutions/products will be used for the core banking/card processing functionality (if there is no partner bank)

What to do:

The key task at this stage is to implement 2 or 3 vertical user operation scenarios, e.g. login, card list view, transfer between cards, etc. You also observe the integration design of all components (front end, core banking, card processing, authentication, and so on). Another vital step here is the creation of the UI/UX design.

Once a minimum set of features required to go live is ready, early adopters test the product and give us feedback to improve the solution.

As the leading digital banking vendor, we recommend to include this set of core features:

![]()

(account opening + card)

![]()

(potentially — utility payments)

![]()

(cards, accounts)

![]()

![]()

![]()

*More features can be released at later stages.

The development of digital banking solutions is better off with regular releases of features. This allows your users to see the growth. We advise arranging the backlog and CI/CD processes under the supervision of the dedicated digital banking team. We can help you both with the implementation of digital banking projects and the subsequent handover of the developed online banking platform to your own team. We also can create a joint hybrid team to enhance your software together.

The second vital point is the construction of the service ecosystem. You don't need to develop all services yourself, as many of them are already available. It is important to integrate engaging services into the digital bank's ecosystem for a fast extension of the functionality (e.g., accounting service for SMBs, personal/business finance management, etc).

No need for individual staffing. We have already assembled, balanced, and focused engineering teams ready for onboarding.

Depending on the project conditions and limitations, the team structure and the number of team members may significantly vary. Our engagement shows that the implementation of a middle-sized digital banking project requires the following team members:

![]()

1

Product Owner

![]()

1

Project Manager

![]()

3

System Analysts

![]()

1

Technical Architect

![]()

1

UI/UX Expert

![]()

4

Back-End

Developers

![]()

3

Front-End

Developers

![]()

4

Mobile Developers

(iOS + Android)

![]()

3

QA Engineers

![]()

1

DevOps Engineer

Our company may promptly send you a team profile for digital banking development. We expect to have a lot of questions requiring clarification.

Get insights from our experts on how much financial institutions may pay for the development of a digital bank.

We know how to approach a digital banking project effectively, so we've implemented a set of modules and components as well as some typical architectures. From the technical perspective, they ensure that your scalability, maintainability, performance, and security requirements are met.

We can arrange a white-label implementation of the business logic for a range of components which speeds up the project rollout and cuts risks.

A digital bank may be defined as a set of microservices (however, the microservice architecture is not a must-have).

Services use the messaging integration style.

Mobile and web clients communicate with services via an API gateway.

All services communicate internally via a message broker (Kafka, ActiveMQ, etc.).

Mobile and web employ the REST communication style.

All services have a similar structure (by default) for technology consistency.

No heavyweight containers. Services are based on lightweight runtime (Spring Boot, MicroProfile, Micronaut, Quarkus, or similar).

Services are containerized (Docker).

Services have externalized configuration for easy staging.

Each service has its own database (scheme).

Using the Agile approach, we created a digital banking solution that united mobile and online banking. We lessened the burden on retail banking branches and provided clients with more personalized services via smart analytics.

As a global digital banking provider, we can use any tech from our expertise pool. However, for solutions used by banks and credit unions, we prefer those listed below.

React

Java .NET Scala Go

Swift Kotlin React Native

RabbitMQ ActiveMQ Kafka Kubernetes Docker AWS Azure

PostgreSQL MS SQL

The major advantages of the digital banking platform that we offer are its effective horizontal and vertical scalability. We are able to secure the conformity with the performance requirements in case the load on the system rises due to the upgrade of server hardware and the increase in the number of the server cluster nodes.

To achieve the required number of users we:

To achieve the system response time we:

There are two secure options:

We can go over both alternatives depending on your digital banking platform. As one of the global online banking software providers, we suggest to consider the following factors:

Preferable service-level agreement (SLA)

Inhouse resources and expertise in deployment and system support

Service scaling prognosis (increase in the number of users or operations)

Available hardware resources

Security requirements

Planned staging configuration and CI/CD aspects

Just like with any other type of software, to build a user-friendly payment solution, you need to be aware of all its traps and the best industry practices.

Feel free to get in touch with us! Use this contact form for an ASAP response.

Call us at +44 151 528 8015

E-mail us at request@qulix.com

Feel free to get in touch with us! Use this contact form for an ASAP response.

Call us at +44 151 528 8015

E-mail us at request@qulix.com

![]()

![]()

![]()